Replacing or upgrading an HVAC system in Southwest Florida is rarely cheap. A new central air unit alone can run anywhere from $5,000 to $15,000 installed, and that number climbs fast for commercial properties. Most homeowners and business owners assume they have to either drain their savings or just suffer through a failing system. That assumption is wrong. HVAC financing lets you spread payments over time, keep your cash intact, and often access more energy-efficient equipment than you could afford upfront. This guide breaks down every major financing option available to Southwest Florida property owners, what each one costs, and how to avoid the traps that catch people off guard.

Table of Contents

- What is HVAC financing?

- Common HVAC financing options for homeowners

- Financing options for commercial HVAC projects

- Evaluating costs, savings, and potential risks

- How to apply and get approved for HVAC financing

- Our take: What most Southwest Florida owners get wrong about HVAC financing

- Ready to upgrade? Explore your Southwest Florida HVAC solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| HVAC financing basics | You can spread the cost of HVAC upgrades or replacements using loans, leases, or payment plans tailored for homes or businesses. |

| Homeowner options | Contractor financing, personal loans, and PACE each offer different rates, terms, and benefits depending on your finances and goals. |

| Commercial programs | Business owners can leverage C-PACE and other long-term loans to finance energy upgrades with affordable payments in Florida. |

| Compare and plan | Estimate total costs, watch for interest and liens, and use energy savings or rebates to make upgrades affordable and smart. |

What is HVAC financing?

HVAC financing is simply a way to pay for a heating or cooling system over time instead of all at once. Think of it the way you would a car loan or a home improvement loan. Instead of writing a check for $10,000 today, you make smaller monthly payments over a set period, usually anywhere from 12 months to 20 years depending on the program. HVAC financing spreads payments for system upgrades and installs over time instead of requiring full payment upfront.

Both homeowners and commercial property owners use HVAC financing. On the residential side, it covers central AC units, heat pumps, ductless mini-splits, furnaces, and indoor air quality equipment like air purifiers and dehumidifiers. On the commercial side, the same categories apply but often at larger scale, covering rooftop units, chillers, and full building systems.

Why does financing matter so much in Southwest Florida specifically? Because the climate here is brutal on HVAC equipment. Systems run harder and longer than almost anywhere else in the country, which means they wear out faster and efficiency upgrades have a bigger financial payoff. Financing makes those upgrades accessible before the old system completely fails.

Here are the main reasons Southwest Florida owners turn to affordable HVAC financing solutions:

- Preserve cash flow for emergencies or other investments

- Access higher-efficiency systems that cost more upfront but save more monthly

- Capture tax credits and rebates that reduce the financed amount

- Increase property value without a large lump-sum expense

- Handle unexpected breakdowns without scrambling for funds

Financing works whether you are planning a strategic upgrade or dealing with a system that died on a Friday afternoon in August. The key is knowing which option fits your situation.

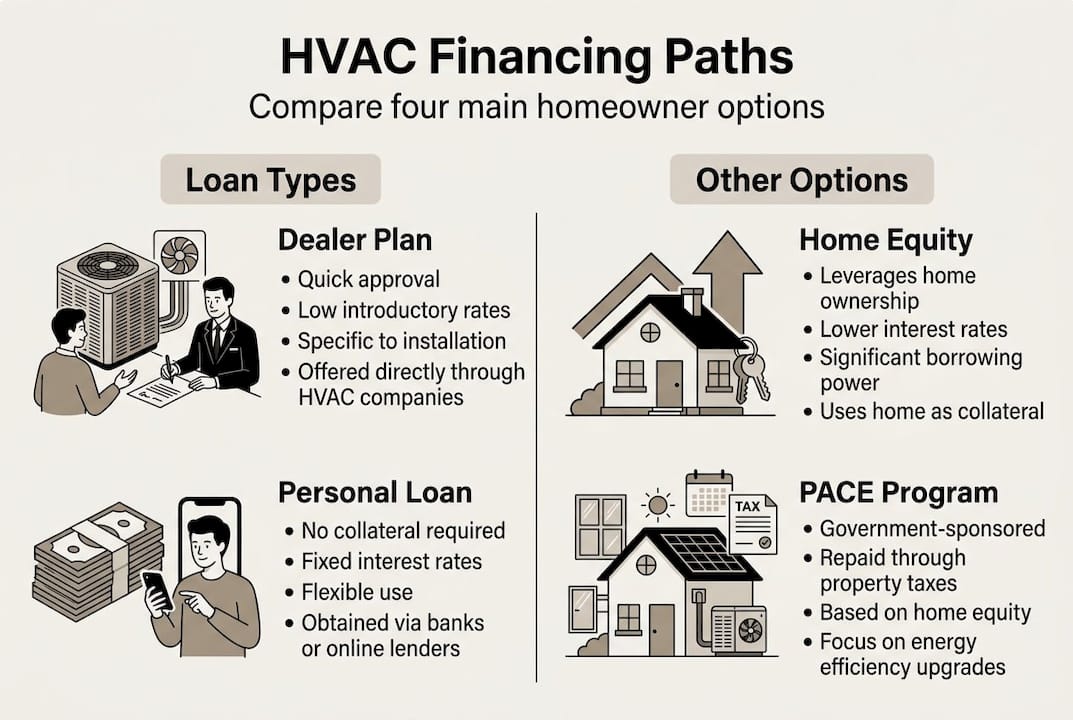

Common HVAC financing options for homeowners

Now that you understand what HVAC financing is, let’s explore the main options homeowners in Southwest Florida can actually use.

There are four primary financing paths for residential customers. Each has different rates, terms, and eligibility requirements. Here is a side-by-side comparison:

| Financing type | Typical APR | Term length | Credit needed | Key advantage |

|---|---|---|---|---|

| Contractor/dealer financing | 0% promo or 18-29% | 12-84 months | 580+ | Fast approval, one-stop shop |

| Personal loan | 7-25% | 24-84 months | 580-660+ | No home equity required |

| HELOC/home equity loan | 6-10% | 5-20 years | 660+ | Lowest rates, tax deductible interest |

| PACE/on-bill financing | 5-8% fixed | 10-25 years | No check | Tied to property, not credit |

Typical APRs and term ranges vary significantly across contractor financing, personal loans, HELOC programs, and PACE options, so comparing all four is essential before you commit.

Here is when each option makes the most sense:

- Contractor financing works best when you need fast approval and can pay off the balance during the promotional window

- Personal loans suit renters or homeowners without enough equity who have decent credit

- HELOC or home equity loans make sense for owners with significant equity who want the lowest long-term rate

- PACE financing fits homeowners who want a long repayment term and do not want a credit inquiry

If your credit score is below 620, do not assume you are out of options. There are HVAC financing for bad credit programs specifically designed for that situation. And before you finalize any financing, check whether you qualify for FPL rebates for new AC units, which can reduce the amount you need to finance in the first place.

Pro Tip: Promotional zero-interest dealer plans sound great, but they often use deferred interest, not true zero interest. If you carry any balance past the promo period, the full retroactive interest (sometimes 26-29%) gets added back to your principal. Only use these plans if you are certain you can pay the full balance before the deadline.

Financing options for commercial HVAC projects

Just as homeowners have choices, commercial properties face unique financing opportunities and incentives.

Commercial HVAC projects typically involve larger systems and larger price tags, which opens the door to financing structures not available to residential buyers. Commercial options emphasize equipment finance agreements, capital leases, term loans, revenue-based financing, and C-PACE programs.

| Financing type | Typical rate | Term | Ownership | Transferable? |

|---|---|---|---|---|

| Equipment finance agreement (EFA) | 5-12% | 2-7 years | Buyer owns | No |

| Capital lease | 4-10% | 3-7 years | Option to buy | No |

| Term loan | 6-15% | 1-10 years | Buyer owns | No |

| Revenue-based financing | Variable | 6-36 months | Buyer owns | No |

| C-PACE | 5-8% fixed | 20-30 years | Buyer owns | Yes |

C-PACE (Commercial Property Assessed Clean Energy) stands out from every other option on this list. Here is why:

- No down payment required, covering up to 100% of project costs

- Repayment is tied to the property tax bill, not the business’s cash flow

- Terms stretch 20 to 30 years, making monthly payments very manageable

- The obligation transfers with the property if you sell, which is a major advantage for investors

- No personal credit check in most cases

Florida is one of the strongest states in the country for C-PACE adoption, and Southwest Florida commercial owners are increasingly using it for major commercial HVAC efficiency upgrades. Staying current on Florida HVAC financing trends helps commercial owners time their upgrades to capture the best available programs. For businesses planning larger expansions, business HVAC upgrades can often be bundled into broader facility improvement financing.

Stat to know: C-PACE financing can cover commercial HVAC projects for 20 to 30 years with zero down payment, making it one of the most accessible large-scale upgrade tools available to Florida business owners today.

Evaluating costs, savings, and potential risks

The next step is to make sure you understand the real numbers and potential pitfalls before you commit.

Here is a step-by-step process for estimating your true cost with financing:

- Get your system price. A standard residential install in Southwest Florida runs $5,000 to $15,000. Check new AC unit costs for current Naples-area pricing.

- Calculate your monthly payment. A $10,000 system financed at 9% over 60 months runs approximately $208 per month.

- Subtract rebates and credits. IRA tax credits can reduce your net cost by $600 to $2,000 depending on the equipment.

- Factor in energy savings. A new high-efficiency system can cut your monthly utility bill by 20 to 50%, which partially or fully offsets your payment.

- Model the worst case. If you miss a promo payoff deadline, recalculate with the full deferred interest added back.

Average system costs and payment calculations show that interest charges can add thousands to your total if a promotional period expires unpaid, so modeling both scenarios is critical before signing.

A $10,000 system at 9% for 60 months costs roughly $208/month. With a $2,000 IRA tax credit and $80/month in energy savings, your real out-of-pocket cost drops to under $130/month. That is less than most people spend on a streaming subscription bundle.

The main risks to watch for include deferred interest traps on promo plans, PACE liens that can complicate refinancing or a home sale, and lease agreements where you never actually own the equipment. Adding HVAC zoning for savings to your upgrade can push energy savings even higher, improving your payback timeline.

Pro Tip: Before signing any financing agreement, ask your installer to show you the projected monthly energy savings in writing. A reputable contractor will provide this. If they cannot, that is a red flag.

How to apply and get approved for HVAC financing

After you have evaluated your costs and chosen the best financing pathway, here is how to move forward and secure your approval.

Follow these steps to give yourself the best shot at fast approval and favorable terms:

- Choose your installer first. Many financing programs are tied to specific contractors. Work with a licensed Southwest Florida HVAC company and ask what programs they offer. Review the HVAC financing process in Estero as a local example of how the process flows.

- Get at least two proposals. Compare system options, efficiency ratings, and financing terms side by side before committing.

- Pull your credit report. Know your score before applying. Credit requirements by financing type typically start at 580+ for personal loans and 660+ for home equity options, while PACE programs usually skip the credit check entirely.

- Gather your documents. Most lenders want proof of income, a recent utility bill, and property ownership documents. Commercial applicants may also need business financials.

- Apply for incentives simultaneously. File for IRA tax credits and utility rebates at the same time you apply for financing so you can reduce the financed amount from the start.

- Read the fine print. Look specifically for deferred interest clauses, balloon payments, lien language, and ownership terms before you sign anything.

If a system breaks down unexpectedly, the HVAC repair steps guide can help you decide whether repair or full replacement with financing makes more financial sense in your situation.

Our take: What most Southwest Florida owners get wrong about HVAC financing

Now, let’s step back and look at what most people overlook when financing HVAC upgrades in Southwest Florida.

The single biggest mistake we see is homeowners choosing a contractor’s promotional zero-interest plan simply because it sounds like a great deal, without fully understanding the deferred interest risk. Contractor promo financing is risky for anyone who cannot guarantee they will pay off the full balance within the promotional window. Life happens. Unexpected expenses come up. And when they do, that “zero percent” plan can suddenly become a 26-29% interest charge applied retroactively to your original balance.

Government-backed programs and fixed-rate loans do not come with the same marketing appeal, but they deliver far more predictable outcomes for the majority of property owners. A fixed 8% loan over 7 years is less exciting than “zero percent for 18 months,” but it is far less likely to blow up your budget.

For owners with credit challenges, affordable options for bad credit are more accessible than most people realize, especially through PACE programs.

Pro Tip: Always model the worst-case scenario, not just the best case. Get every term in writing and ask specifically: “What happens to my rate if I miss the payoff deadline?” The answer to that one question will tell you everything you need to know.

Ready to upgrade? Explore your Southwest Florida HVAC solutions

Having explored the essentials and nuances of HVAC financing, here is how you can put that knowledge to work with a team that knows Southwest Florida’s climate and your options inside out.

At Ultra Air Heating & Cooling, we work with homeowners and commercial property owners across Naples, Cape Coral, and Fort Myers to match the right system with the right financing. Whether you need heating solutions, want to improve your indoor air quality solutions, or are trying to figure out which of the many HVAC systems for Florida homes fits your property best, we can walk you through every option. Schedule a free consultation today and let us help you find a payment plan that makes comfort affordable without the guesswork.

Frequently asked questions

What credit score do I need for HVAC financing?

Most HVAC financing requires a score of 580+ for personal loans and 660+ for home equity options, but PACE programs in Florida often skip the credit check entirely, making them accessible to a much wider range of applicants.

Are there zero interest HVAC financing options?

Yes, many contractors offer zero-interest promotional plans for 12 to 18 months, but interest rates can jump to 26 to 29% retroactively if the balance is not paid in full before the promotional period ends.

What can I finance with an HVAC loan?

Most programs cover AC units, heat pumps, furnaces, installation labor, and sometimes indoor air quality upgrades, as financing covers HVAC installs and related equipment across both residential and commercial projects.

Does HVAC financing affect my mortgage if I sell my home?

PACE liens and some loan types can complicate a home sale or refinancing, so always confirm in writing how the obligation transfers and discuss the implications with your mortgage lender before signing.

Are there rebates or tax credits that help with HVAC financing?

Southwest Florida residents may qualify for up to $2,000 on heat pumps or $600 on qualifying AC units and furnaces through IRA tax credits in 2026, plus additional savings through local utility rebate programs.

Recommended

- HVAC Financing for Bad Credit in Naples: Get Your AC Running Today – Ultra Air Heating and Cooling

- HVAC Financing Options in Estero, FL: Your 2026 Guide to Affordable Comfort – Ultra Air Heating and Cooling

- Florida HVAC Trends: Boost Efficiency and Comfort in 2026

- What is HVAC zoning? Improve comfort & cut costs

- solar panel financingFinancing Options – Shepherd Electrical